Scope 1, 2 & 3 Emissions: What Auditors Expect

As climate reporting requirements tighten, auditors are applying greater scrutiny to Scope 1, Scope 2, and Scope 3 emissions. Organisations are now expected to prepare emissions data with the same discipline, controls, and transparency as financial information. This article explains what auditors typically expect when reviewing Scope 1, 2, and 3 emissions, common assurance issues, [&

Australia’s Mandatory Climate Disclosures Explained: What Organisations Need to Know

Australia has introduced mandatory climate-related financial disclosures, marking a significant shift in how organisations must identify, manage, and report climate risk. These requirements move climate reporting from a voluntary sustainability exercise to a regulated financial and governance obligation. This document explains: Why Australia Introduced Mandatory Climate Disclosures C

How to Prepare Emissions Data for External Assurance

As emissions reporting becomes more regulated and scrutinised, external assurance of emissions data is increasingly expected by regulators, investors, and boards. Preparing for assurance is not a final-stage activity—it requires structured data, consistent methodologies, and clear governance throughout the reporting cycle. This guide explains how to prepare emissions data for exter

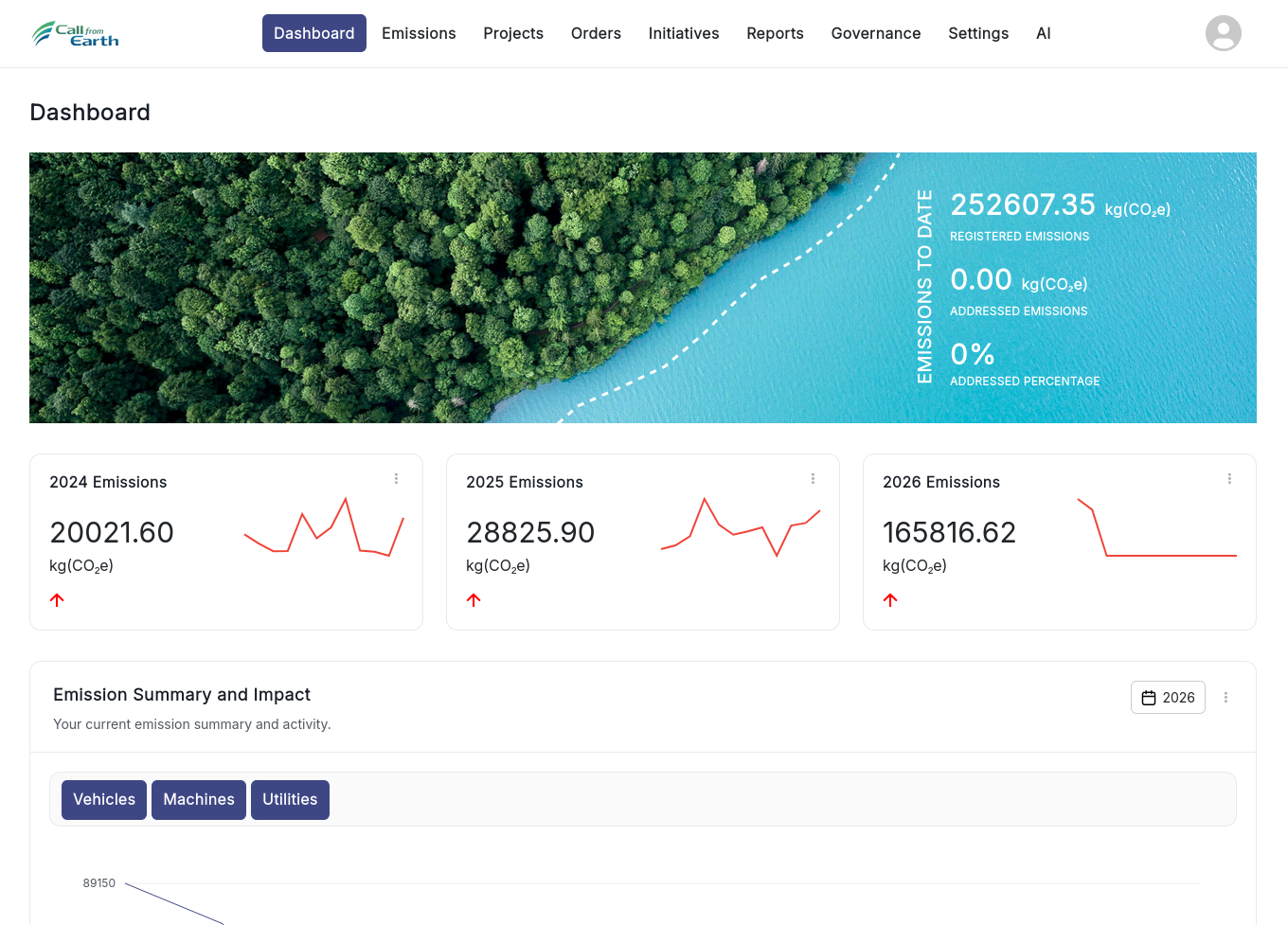

Why Auditors Recommend Emissions Platforms such as Call from Earth for Scope 1, 2 & 3 Audits

As sustainability reporting shifts from voluntary disclosure to mandatory, externally assured reporting, organisations are under increasing pressure to demonstrate not only accurate Scope 1, Scope 2, and Scope 3 emissions data, but also a clear understanding of the climate-related risks and opportunities associated with those emissions. Auditors are no longer reviewing emissions numb